進口代理—美國關島—「美國關島觀光局」投資環境諮詢與產業趨勢分析

- 發布日期:

- 瀏覽人次:

7

- 公司名稱:美國關島觀光局

- 公司所在:

- 產品/技術:關島投資環境諮詢與產業趨勢分析

- 官網:https://www.visitguam.org.tw/

- 產業別:稅務,金融外匯,經貿法規,通關物流

關島投資環境諮詢與產業趨勢分析

The Guam Taiwan Office represents the official economic promotion entity of Guam in Taiwan. It promotes Guam as a facilitator of cooperation in investment and cultural exchange between Guam and Taiwan.

關島台灣辦事處為關島在台官方經貿推廣機構,主要促進關島與台灣之間在投資及文化交流等領域的合作。

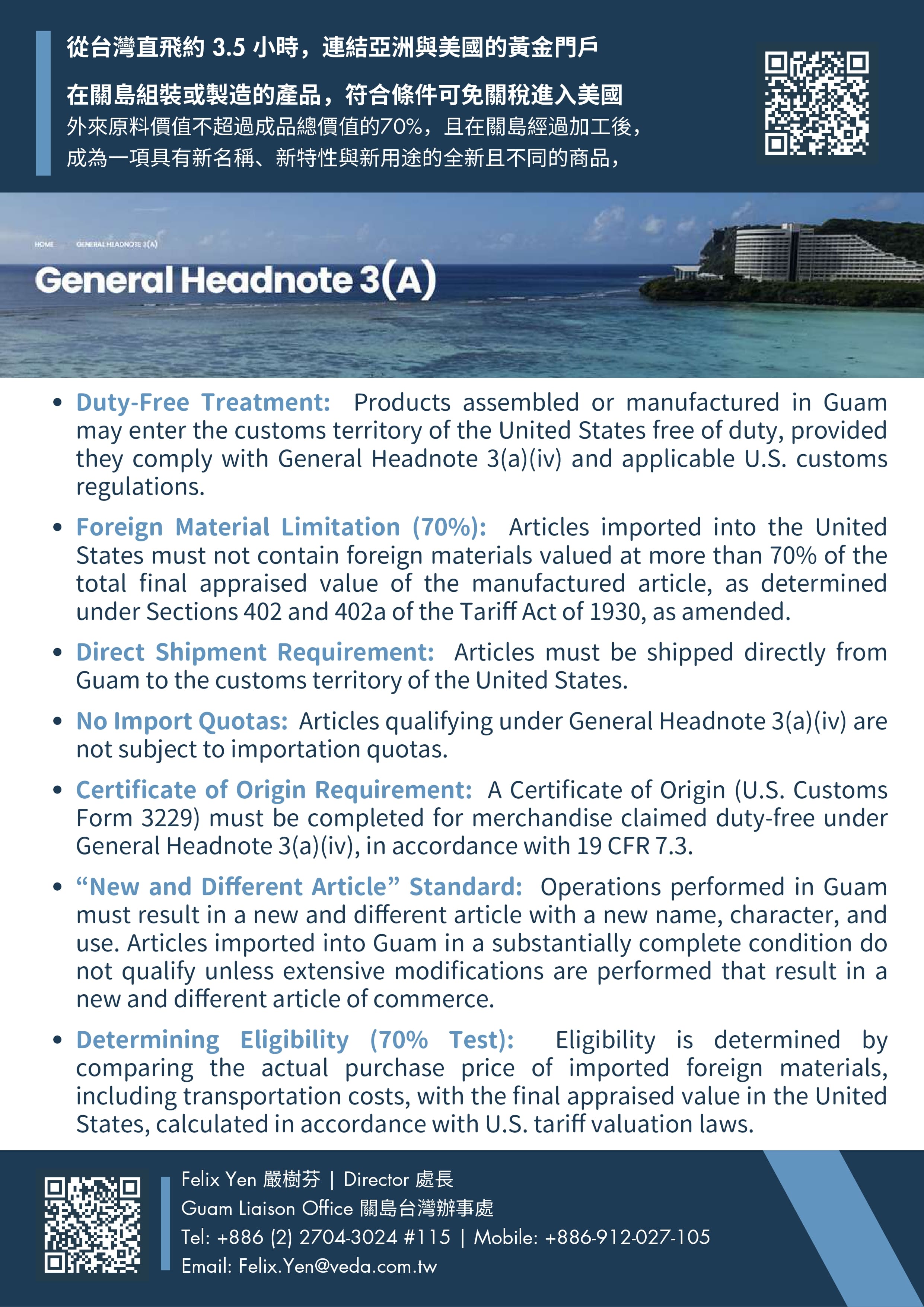

General Headnote 3(A)

1. Duty-Free Treatment

Products assembled or manufactured in Guam may enter the customs territory of the United States free of duty, provided they comply with General Headnote 3(a)(iv) and applicable U.S. customs regulations.

2. Foreign Material Limitation (70%)

Articles imported into the United States must not contain foreign materials valued at more than 70% of the total appraised value of the manufactured article, as determined under Sections 402 and 402a of the Tariff Act of 1930, as amended.

3. Direct Shipment Requirement

Articles must be shipped directly from Guam to the customs territory of the United States.

4. No Import Quotas

Articles qualifying under General Headnote 3(a)(iv) are not subject to importation quotas.

5. Certificate of Origin Requirement

A Certificate of Origin (U.S. Customs Form 3229) must be completed for merchandise claimed duty-free under General Headnote 3(a)(iv), in accordance with 19 CFR 7.3.

6. "New and Different Article" Standard

Operations performed in Guam must result in a new and different article with a new name, character, and use. Articles imported into Guam in a substantially complete condition do not qualify unless extensive modifications are performed that result in a new and different article of commerce.

7. Determining Eligibility (70% Test)

Eligibility is determined by comparing the actual purchase price of imported foreign materials, including transportation costs, with the final appraised value in the United States, calculated in accordance with U.S. tariff valuation laws.

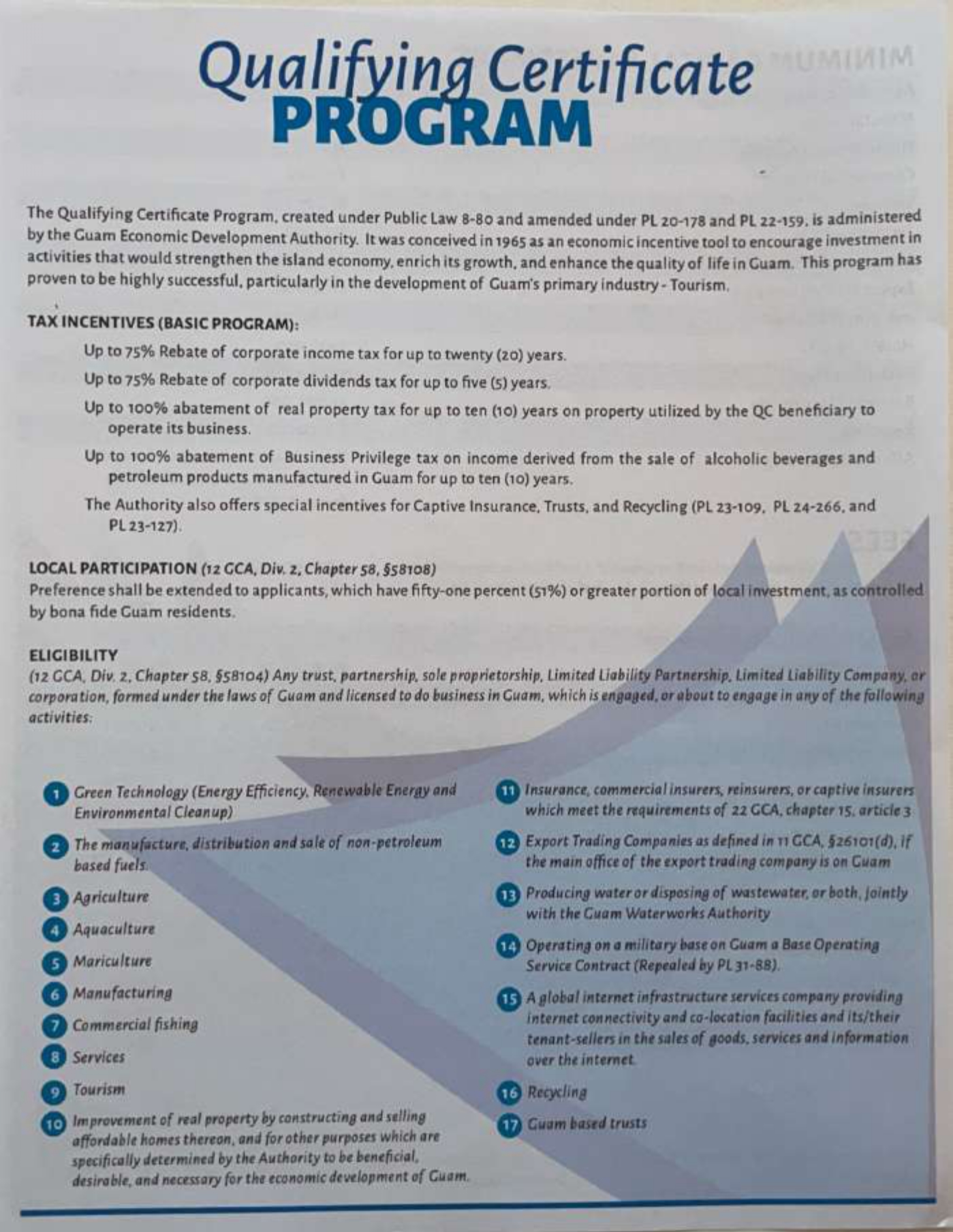

QC Program

1. Program Overview

- Purpose: To encourage investment in activities that enrich Guam's growth, particularly within the tourism industry.

- Legal Basis: Created under Public Law 8-80 and subsequently amended by several other Public Laws.

2. Tax Incentives (Basic Program)

The program offers significant tax breaks to eligible beneficiaries:

- Corporate Income Tax: Up to a 75% rebate for up to 20 years.

- Corporate Dividends Tax: Up to a 75% rebate for up to 5 years.

- Real Property Tax: Up to 100% abatement for up to 10 years on property used for the business.

- Business Privilege Tax: Up to 100% abatement for 10 years on income from Guam-manufactured alcoholic beverages and petroleum products.

- Special Incentives: Specific benefits are available for Captive Insurance, Trusts, and Recycling.

3. Local Participation

Preference is given to applicants where 51% or more of the investment is controlled by bona fide Guam residents.

4. Eligibility

Any legal business entity (trust, partnership, LLC, corporation, etc.) licensed in Guam is eligible if they engage in one of the 17 specified activities, which include:

- Green Technology (Renewable energy, environmental cleanup).

- Agriculture & Mariculture (Commercial fishing, aquaculture).

- Manufacturing & Services.

- Tourism.

- Affordable Housing Development.

- Global Internet Infrastructure Services.

- Insurance & Guam-based Trusts.

- 聯絡人:Mr. Felix Yen嚴樹芬; Ms. Sarah Huang 黃姝誼

- 電子信箱:Felix.Yen@veda.com.tw; sarah.huang@veda.com.tw

- 聯絡電話:0912027105; 02 2704 3024